Business model & Tokenomics

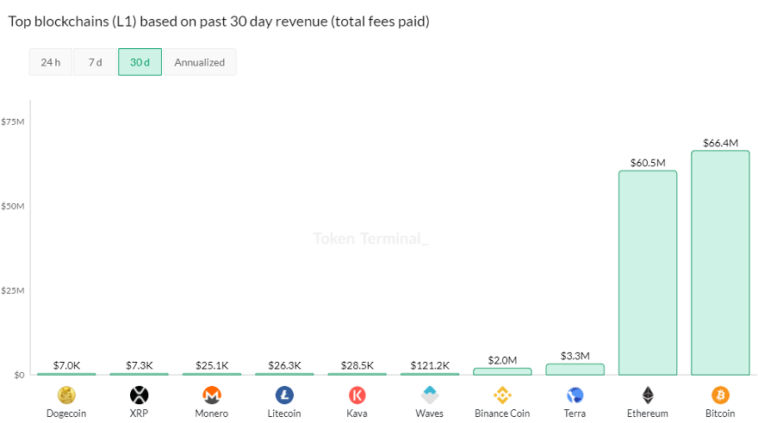

Terra is a set of stablecoins pegged to national currencies for payments in e-commerce. Merchants who accept Terra get paid in 6 seconds and pay 0,6% fee in comparison to current 7-day settlement period and 2,8 % credit card fee. In November, Terra processed $330m of payments volume resulting in approximately $3,3m revenue. As such, Terra is the 3rd most revenue generating blockchain after BTC and ETH (source: TokenTerminal).

Currently, most transaction fees are collected via the 2m+ users of a popular South Korean e-commerce payment application CHAI. The more ecommerce purchases settled via CHAI, the more revenue will be shared with the stakers.

The LUNA token acts as dividend-yielding equity because the token holders receive 100 % of the transaction fees (if staked). Currently, around 28,9 % of LUNA holders stake the token and receive 10,37 % of annualized yield (source: TerraStation).

Source: Tokenterminal

Valuation

Key Information

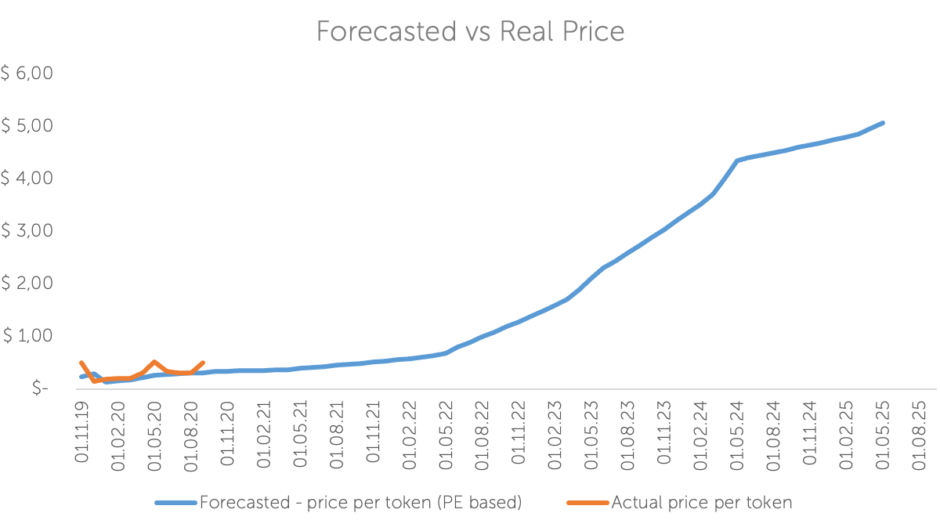

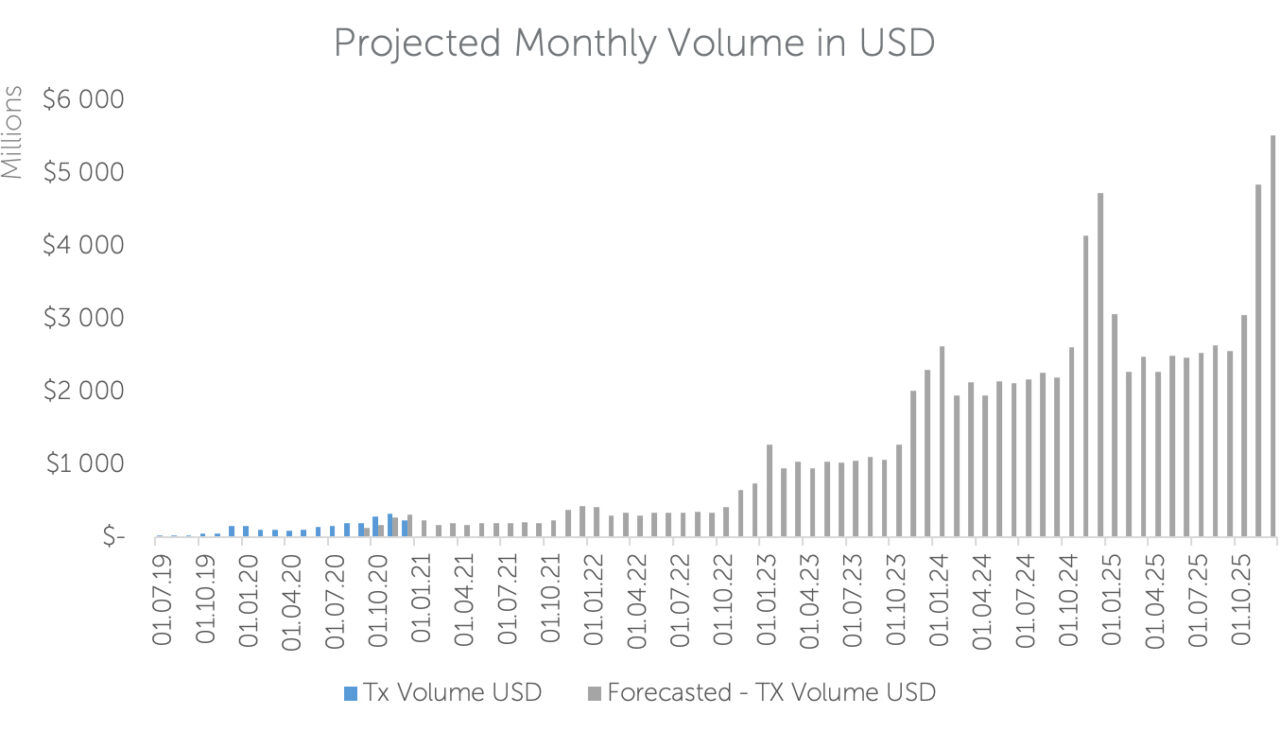

We assume that Terra will process about $3bn average monthly volume in 2025, which is $36bn per year in 2025. Terra experienced significant growth over the past year. Last year in October, they processed $58.8m per month, this year in October they processed $283m per month (4,8x). Similarly, past year in November Terra processed $55,4m, whereas this November the growth continued, and they facilitated $330m (5x) in transactional volume.

We assume that Terra will process about $3bn average monthly volume in 2025, which is $36bn per year in 2025. Terra experienced significant growth over the past year. Last year in October, they processed $58.8m per month, this year in October they processed $283m per month (4,8x). Similarly, past year in November Terra processed $55,4m, whereas this November the growth continued, and they facilitated $330m (5x) in transactional volume.

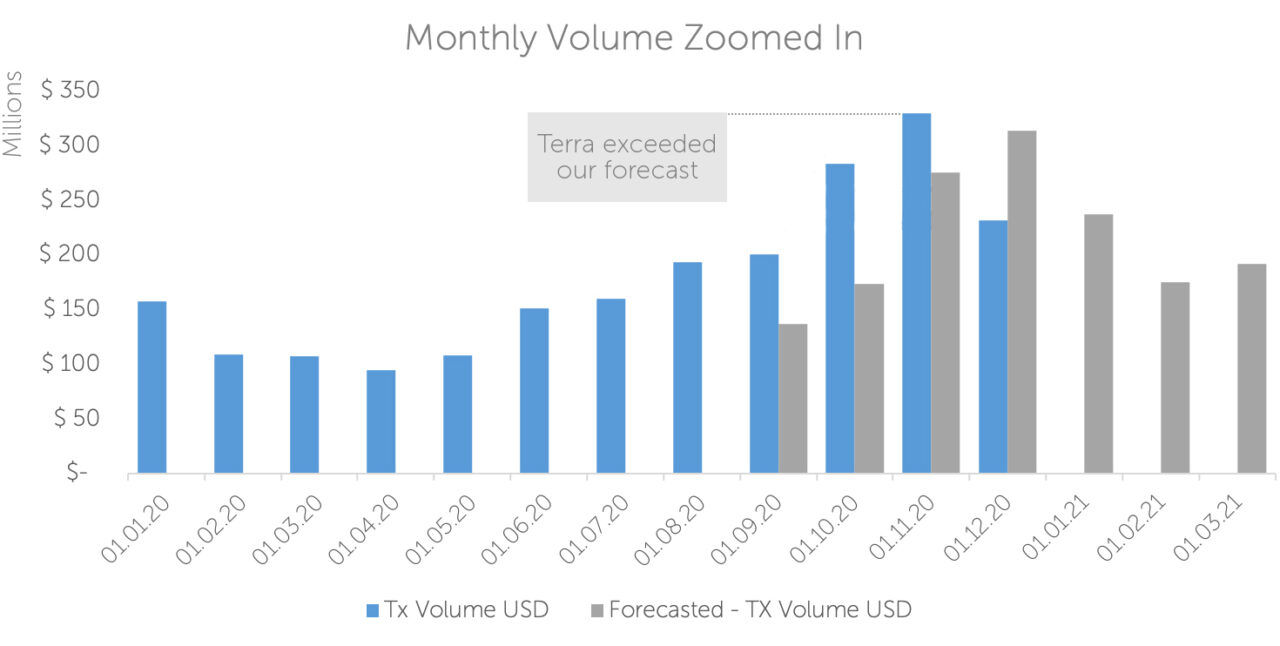

*Figures in 2020 are partially actual data and partially our forecasts for the rest of 2020. Past 2020, all data is our forecast.

We have modeled the monthly volume until Dec. 2025 using S-curve and applied seasonality from a similar e-commerce business based in Europe. Our scenario is more conservative than the target of the Terra management team. Terra targets to reach $75bn volume in 2025, we project $36bn.

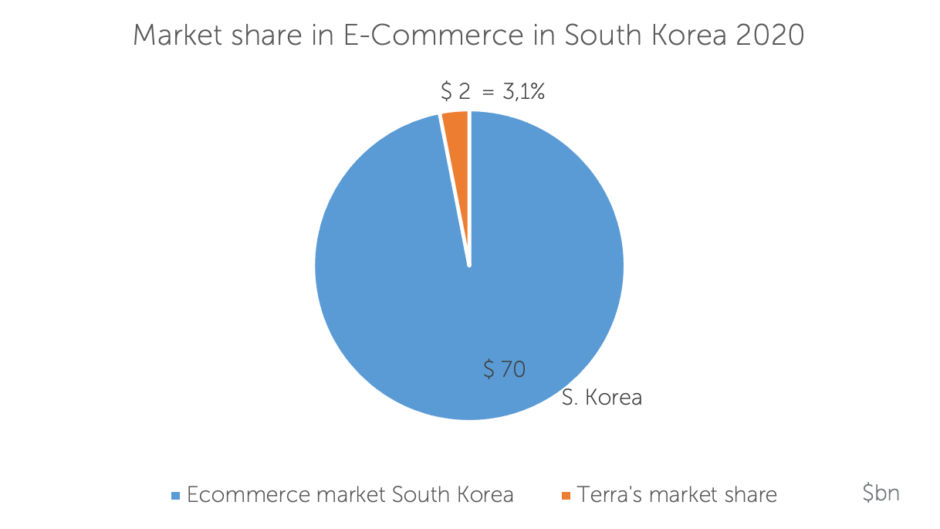

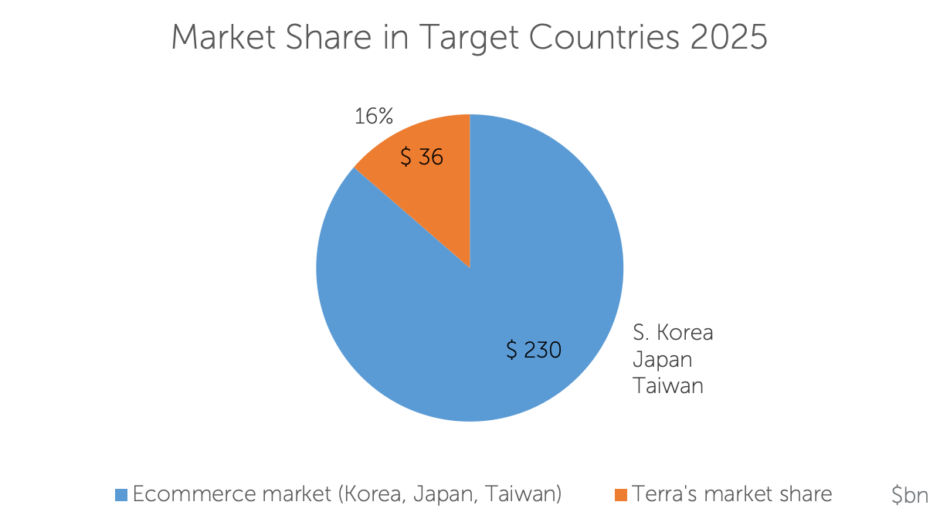

$36bn in transaction volume in 2025 would mean that Terra reached 16% of the e-commerce market in South Korea, Japan and Taiwan (total e-commerce market in those 3 countries is $230bn).

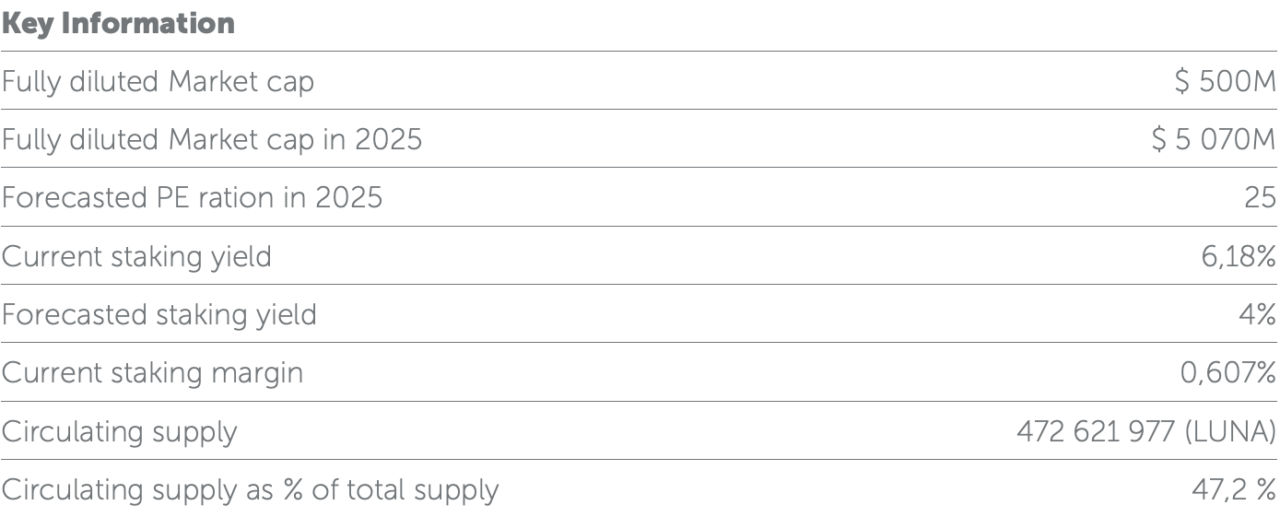

In 2025, fees of $200m would result in a fully diluted market cap of $5bn, based on relatively conservative PE ratio 25. Note: PayPal has 52 PE (TTM) ratio and Visa has 42 PE ratio. Market cap of $5bn would result in the $5.07 exit price per token.

Currently, Terra is exceeding our scenario forecasts by 40-60 % during the past 3 months. Our forecast includes revenue only from already released products; it does not consider revenue from planned products like Anchor and Mirror. Anchor is a stable yield, low risk savings protocol that has been announced but not yet released. Mirror enables trading of representations of US equities on blockchain. On top of CHAI, these new products could be the future drivers of growth. Mirror and Anchor could see fast adoption when CHAI integrates them natively and offers the products to the 2m+ users. On the other hand, Mirror and Anchor do not have traction yet and the cash flow generated by them is highly uncertain.

Sources: Internal analysis Rockaway Blockchain Fund

Traction

1. CHAI

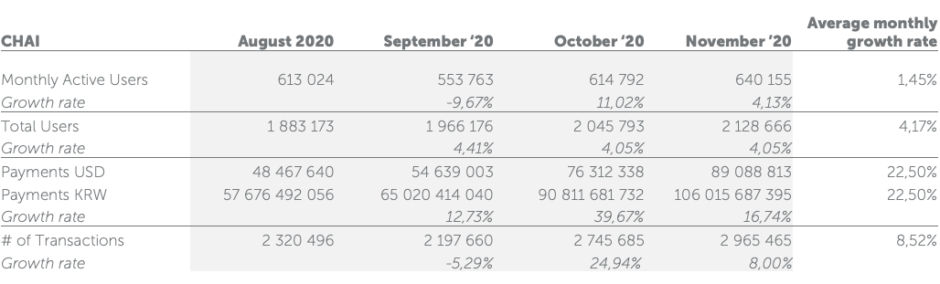

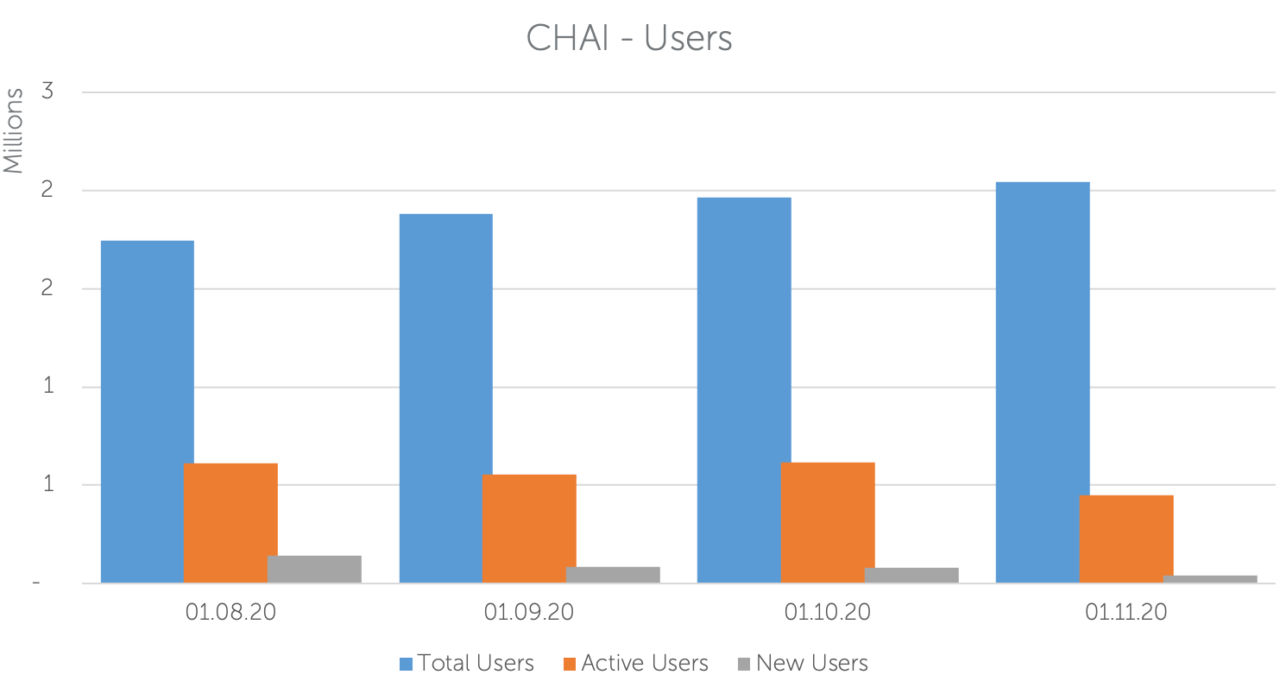

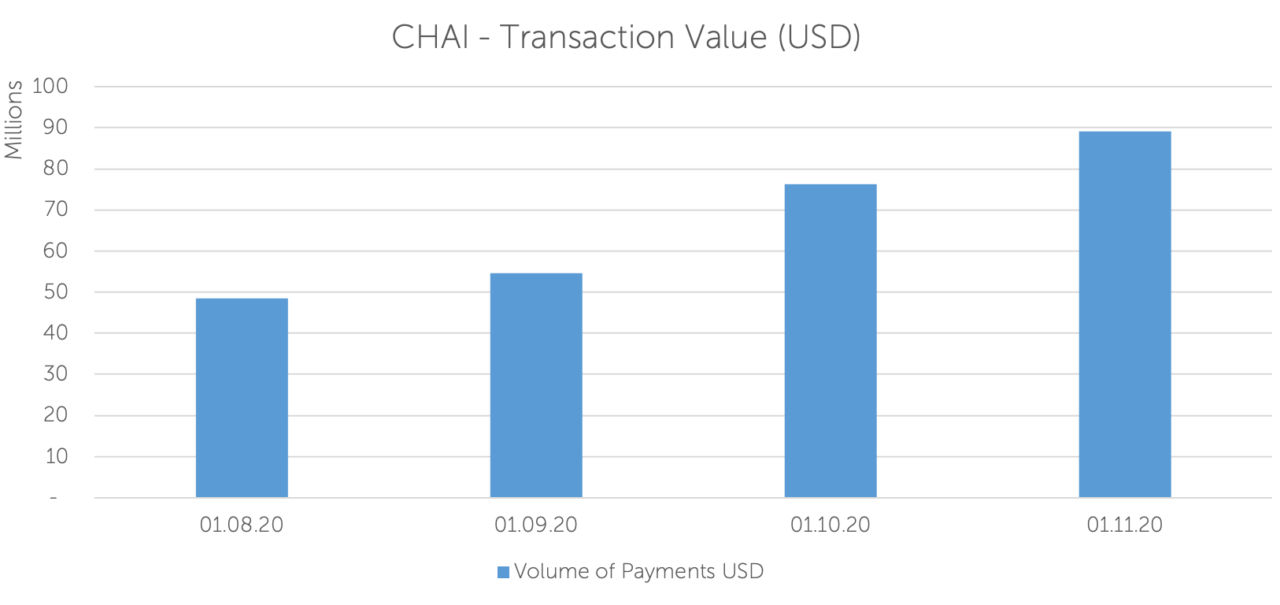

E-commerce payment application CHAI has the most traction in the Terra’s ecosystem with more than 2,4m monthly transactions and 2m+ users. CHAI has approximately 300k weekly active users and 15k new users per week. We expect that the number of users will continue to increase as the company strives for expansion into Japan and Taiwan.

Source: CHAI scan

2. Mirror

Mirror is a newly launched product, that creates representations of US equities on Terra’s blockchain. These newly created derivatives can be traded natively both on Mirror and on Uniswap. Both exchanges are automated market-maker based exchanges.

On Mirror, any user can buy or sell the synthetic assets. A user can also enter a net short position on an asset by locking-in collateral and issuing the asset. At launch, Terra’s UST will be the only accepted stablecoin as collateral. Other Terra’s stablecoins are expected to be added later.

Product native token, MIR acts as a governance token with a CF associated with it. When the synthetic derivatives are traded on Mirror, 0,3% fees will incur. 0,25% goes to liquidity providers and 0,05% goes to the MIR token holders.

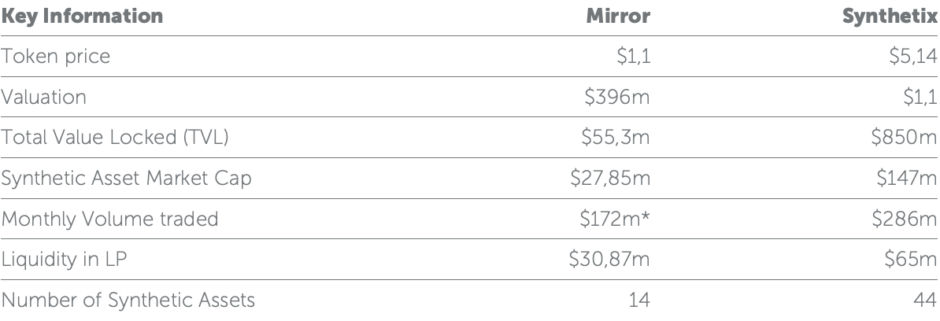

There is a fixed supply of 360m MIR tokens. Based on the current price of MIR $1,1 the fully diluted market capitalization of Mirror is $396m. The product has been live since 4th of December 2020.

Currently available solutions for trading equities representations on blockchain are Synthetix and FTX. Synthetix, requires 750 % minimum collaterization ratio, whereas Mirror Mirror requires only a minimum of 150% collateralization ratio, thus achieving higher capital efficiency. Mirror also offers persmissionless non-custodial solution, whereas FTX’s solution is based on the company holding in custody real shares and issuing a claim on the underlaying asset on blockchain. This claim is fully reserved and redeemable on request.

If Mirror is successful, it will drive demand for Terra’s stablecoins. Higher demand for stablecoins is linked to increasing value of LUNA token via the process called seigniorage described further down.

* Data extrapolated based on 7th of December traded volume.Source: https://terra.mirror.finance/ and https://stats.synthetix.io/

Team

Do Kwon (CEO)· Founder and ex-CEO of Anify.· Stanford University Alumni

Daniel Shin (COO of Terra, CEO of CHAI)· Serial entrepreneur for 9 years· Founded TMON e-commerce business with $3,5bn revenue.· Past experience at McKinsey and JPMorgan Chase

The team has a both blockchain and e-commerce industry experience. Terra also succeeds in attracting talent from top employees such as McKinsey and Uber, and tier one universities such as Wharton, Princeton, and LSE.

Investors

Terra raised $32m in seed financing round in 2018 from the above-mentioned investors.According to Cryptorank, Terra also had a $62m ICO at a price of $0,8/LUNA token.

According to Crunchbase, there were several other rounds on top of traditional VC Seed and Series A naming convention. Therefore, the above-mentioned investors invested in a secondary transaction – either in private or in public.

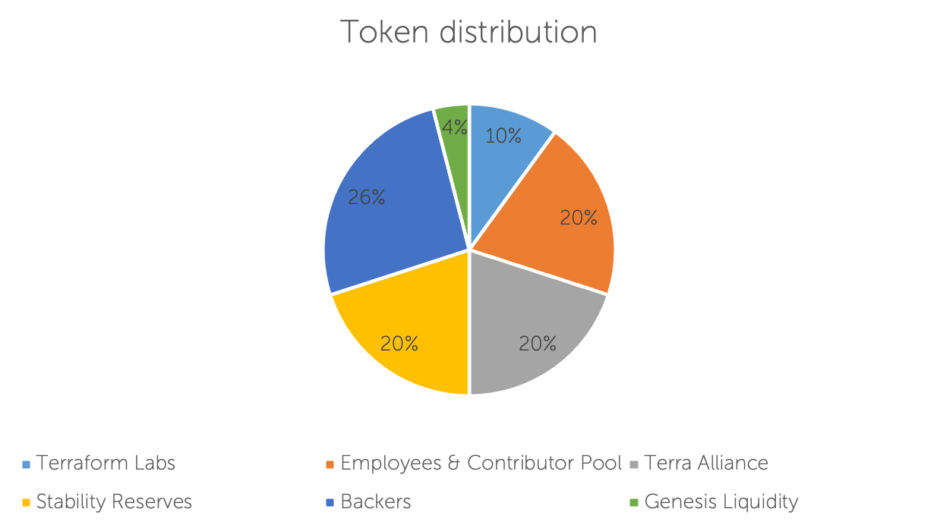

Luna Token

There is 1bn LUNA tokens, which acts as an equilibrium total supply. The tokens will be distributed according to the above outlined distribution. Release schedule of the tokens is not publicly available. Our models count with fully diluted market cap, i.e. it considers maximum dilution as if all tokens were released.

There is 1bn LUNA tokens, which acts as an equilibrium total supply. The tokens will be distributed according to the above outlined distribution. Release schedule of the tokens is not publicly available. Our models count with fully diluted market cap, i.e. it considers maximum dilution as if all tokens were released.

LUNA tokens act as collateral to the stable coins issued on the protocol. LUNA tokens are burned and issued algorithmically according to the demand of stablecoins. The mechanism pressures the stablecoins to maintain their stable value. There are also fees associated with the process of issuing and burning stablecoins (called seigniorage). A proportion of these fees will be distributed to LUNA holders (source Whitepaper). Until $1,3bn worth of stablecoins is emitted, all fees from seigniorage go to the Treasury.

Market and Liquidity

Source: Tradingview (LUNA/USDT on Binance)

In the past 3 months, Terra has traded as high as $0,55 per LUNA token. More recently, the price of LUNA has risen back to $0,5.

Source: Coingecko

Source: Coingecko

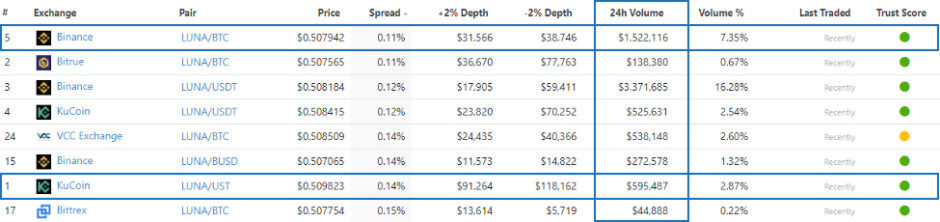

The most traded pair is on Binance exchange with $5,5m 24h volume across 4 pairs. The best spread is also to be found on Binance, reaching 0,11 %. Liquidity measured by the order book depth is the best on a KuCoin’s LUNA/UST pair. Therefore, KuCoin is the most suited exchange for large market order trades.

Risks

There is a legal risk associated with the issuance of LUNA and other stablecoins on Terra blockchain because the regulatory landscape is constantly changing. Adverse regulatory changes might have negative material impact on Terra because they issued $1.3bn of synthetic FIAT money.

Business risk consists mostly of failure of international expansion and failure of bringing new products to market successfully. Also, there are already solutions for merchants that charge much less fees than 0,6%. However, most of the competitors are not active in South Korea.

Conclusion

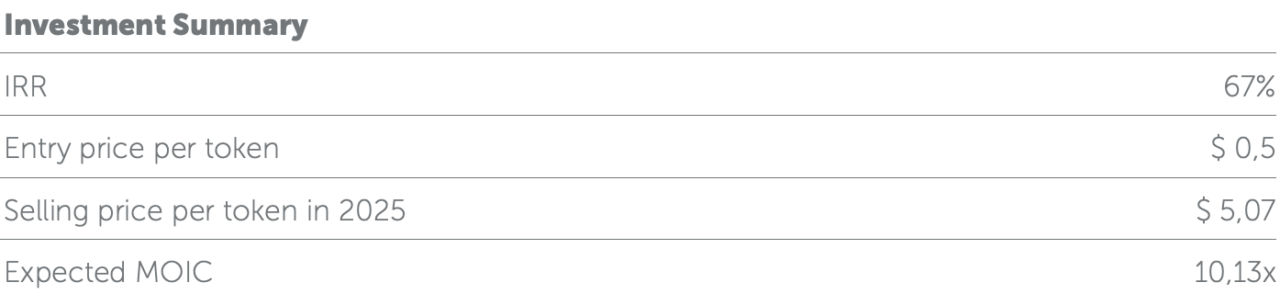

Considering the dividends from staking plus the exit value at the end of 2025, we think LUNA at $0,35 is undervalued. Our model shows a price of $5 by 2025 (10,13xMOIC, 67% IRR including dividends).

We believe our valuation is still conservative because we account only for main product (Terra as a platform for e-commerce payments). We do not account for new projects the team is working on, like Anchor and other possible products in the pipeline. These products are scheduled to come live in the next quarter and if successful, they would produce additional cash flow to the stakers.

Stakers of LUNA also receive pro-rata share of the transaction fees paid by e-commerce merchants, generally around 10 % p.a. As such, LUNA acts as a high dividend growth investment.

All in all, we believe LUNA token is currently a good investment opportunity mainly because the project has a significant traction and has real world usage. We expect the traction to continue and believe Terra will gain more market share in the key Asian markets.

___

Special thanks go to Mike Arrington (partner at Arrington XRP Capital), Do Kwon (Co-Founder of Terra) and Viktor Fischer (partner at Rockaway Blockchain Fund), with whom parts of the analysis were discussed.

Disclaimer:

This article is for informational purposes only, it is not an investment advice and we disclaim any and all our liability for the provided information. It involves a number of assumptions, risks, uncertainties and other statements; actual results may differ materially from such statements. No representation or warranty (expressed or implied) is made as to, the fairness, accuracy, completeness or correctness of the provided information or opinions contained in this article and nothing contained in this article should be relied upon as a promise, representation or indication of the future performance of any asset. Any information contained in this article does not constitute an offer or invitation to purchase or subscribe for any interest in any asset and no part of it shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. Any logos and trademarks are displayed in this article for information/educational purposes only and do not constitute any endorsement of any offering or any investment product

David Rakusan is Investment Manager at Rockaway Blockchain Fund, responsible for portfolio management. He previously worked as an Investment Analyst at RSJ Investments, a financial group with €500M in assets under management, where he was responsible for analyzing both direct investment opportunities and indirect fund of funds investments in the VC sector. David holds a a Master’s Degree in Finance and Financial Management Services from the University of Birmingham and a CFA charter.